Renewable Energy

Tax Equity

Introduction to Tax Equity

If you are a profitable business or a high net worth individual, you need to be familiar with the concept of tax equity. It allows you to take money you normally would use to pay your tax bill and instead invest that money in qualified projects. In exchange, the IRS gives you a tax credit to reduce your bill by roughly that same amount. For those that qualify, it’s a very low risk way to keep more of your cash while helping the environment. This page will help you understand how it works, the benefits, and the risks. (Note that some details have been simplified for ease of understanding.)

While we recommend you read through this page in order, you may jump to any section using the links to the right. If you have any questions or are interested in exploring if tax equity is right for you, please contact us.

Tax Equity Basics

How it works

Let’s say you have a $100 federal tax bill. Normally you’d simply pay that money to the IRS and be done. This results in a net loss of $100. With tax equity, however, you have another option. Instead of paying the IRS your $100, you can invest it into a qualified project. In exchange, the IRS will reduce your tax bill by $100 via a tax credit, plus you’ll get a preferred return + equity in the project. worth about $15 (so net loss of $85). In other words, instead of paying the money to the government, you’re investing that money into a project that gives you a return. Basically you're 'making' ~$15 for free

In the above example, you’re still out $85… but that’s $15 less that you would be if you just paid it in tax. The important point here is that the $100 you invest in the tax equity project wasn’t money you could invest in anything else: the only other alternative was to pay it in taxes.

If you’re a high net worth individual, you can reduce your tax bill, invest in renewable energy, and get a return on money that you would have had to spend on taxes anyway.

If you’re a corporation, your can immediately boost your EPS while also contributing to your ESG mandate. After the end of a 5 year holding period (mandated by the IRS), the sponsor of the project will buy your equity out so it doesn’t remain on your books.

Is this real?

Yes. The energy tax credit is clearly spelled out in Section 48 of the federal tax code. The paraphrased version says:

”...the energy credit for any taxable year is the energy percentage of the basis of each energy property placed in service during such taxable year...the energy percentage is...30 percent...”

Many corporations do this all the time. Here’s a recent article on Bank of America (NYSE: BAC) investing in tax equity projects built at Wal-Mart. Here’s a recent press release on NelNet (NYSE: NNI) investing $11 million in tax equity projects.

Who is eligible for this?

If you’re a corporation with a tax liability, you’re eligible.

For individuals, these tax credits can be used to offset passive income (and possibly active income if you're actively involved in renewable energy and/or real estate). Of course as with most tax things it depends on the person's exact situation. Passthrough entities can also invest, but then the credits just ultimately flows through to the taxable entities anyway.

OK, I’m interested. Tell me more.

Here’s how it works at a high level: say you want to invest $100. We’ll find you one or more qualified projects to invest that $100 in. We’ll manage all of the legal and financial aspects, as well as oversee the construction, operation, and maintenance of the solar project. You’ll simply receive cash flows from the project and a K-1 (which will include the tax credits). Here’s an simplified example spreadsheet of how the credits and cash for a project might look.

For more detail on exactly how the process works, keep reading.

How It Works:

A Step-By-Step Guide

In this section we’ll go deeper into the full lifecycle of a tax equity project, where the tax equity investor gets involved, how the tax credit actually works, and how the deal is structured. This gets into a good amount of detail, but should give you good sense for how it all works. That said, even this section simplifies a few things to make it easier to understand; obviously all of the nuances can be explained if you’re interested in talking further.

Step 1: Developer Secures Site & Project Financing

After the Developer secures the site for a project, they finance construction via construction loan and their own equity. The project itself is owned by an LLC - let’s call it “Project Owner, LLC” and refer to it as the “ProjectCo”.

Step 2: Developer Sets up Partnership

For reasons that will become clear as we go through this, the Developer also sets up a separate LLC taxed as a partnership. This entity is where the tax equity investors will invest, and which will eventually buy ProjectCo. Because this entity will eventually hold the ProjectCo, let’s call this partnership entity HoldCo, LLC. There’s nothing in it to begin with, this is just a shell owned by the Developer.

Step 3: Project Development

The Developer continues development of the project. This step is typically what you’d consider the ‘construction’ of the project: actually building the scaffolding, installing the solar panels, batteries, and electrical support systems, etc.

Step 4: Tax Equity Investors Get Involved

Once construction is nearly complete, the tax equity investors get involved. This is where things get a bit more complicated, so we’re going to break it into steps. However, the overall gist is the following:

Tax equity investors invest in HoldCo

HoldCo will then buy ProjectCo (i.e. the entity that owns the project)

The tax credits generated from the project will flow from ProjectCo to HoldCo to the tax equity investor.

There are some additional nuances here, so let’s break it down step by step.

STEP 4a: Project Valuation

Since the goal is to have HoldCo purchase ProjectCo, two things need happen first: (i) a purchase price for ProjectCo needs to be determined; and (ii) HoldCo needs to obtain the funds necessary to purchase ProjectCo at that price.

For step (i) - that is, determining the project price - a valuation needs to be done of the project to determine fair market value (FMV). From the perspective of the tax equity investor, the reason this is so important is because the number of the tax credits you get is based upon the FMV of the project. As of August 2021, this is currently set at $0.30 in federal tax credits for every $1 of FMV. The exact number of credits per dollar of FMV is set by legislation according to a schedule by year. (Note that there may also be state tax credits available as well.)

Because of this - and because valuation of most assets is as much art as science - there is an incentive for both tax equity investors (and Developers who are using those investors’ money to build the project) to ‘inflate’ the value of the project. The risk here is that if the IRS later determines that the value was inflated, they may disallow those tax credits retroactively, saddling the tax equity investor with an unexpected extra tax bill. Therefore, from a tax equity investor’s perspective, the most important thing is to ensure that the project is conservatively valued by a reputable 3rd party experienced in the space. We do this for you.

Step 4b: Financing the Purchase

The next step is for HoldCo to obtain the funds necessary to purchase ProjectCo. Let’s say for ease of math that the tax equity investor wants to invest $300K and that the FMV of the project is determined to be $1M. (Note that this makes the math easy since if $0.30 of tax credits are granted for every $1.00 of project value, then a $1M project will generate $300K of tax credits.)

To make the purchase, the tax equity investor will invest $300K into the HoldCo. Importantly, for this $300K, the HoldCo will allocate the majority (usually 99%) of the economic ownership - i.e. 99% of all income, losses....and tax credits. The reason this is done is to allow the tax equity investor to avail themselves of all of the tax credits (vs the Developer, who often cannot make use of them). The Developer invests the remaining $700K . retains 1% of the cash and income, and remains the manager of the LLC.

You might be curious why the Developer would be willing to do this. As we’ll see later, they Developer gets their rewards down the road in step 7 where we talk about something called the ‘partnership flip’.

[Technical note: Technically, the tax equity investor isn’t required to invest all $300K right away - see the “Advanced” section at the end of this document for more details.]

Step 4c: Purchasing the ProjectCo

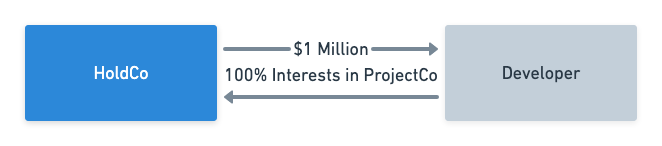

Recall that the project is owned by ProjectCo and that, until now, ProjectCo has been 100% owned by the Developer. Since the FMV of the the project has been determined to be $1M, this means that 100% ownership in ProjectCo is also worth $1M. Therefore at this stage HoldCo pays the Developer $1M in exchange for its 100% ownership in ProjectCo.

The result of the transaction looks like this:

Step 5: The Project is Placed in Service

After this transaction is completed - and only after - does the project get ‘turned on’ to start producing power and selling it. This is called being “placed in service”. The reason for this sequencing is that the tax code states that the tax credits given to this project are allocated based upon the ownership of the project at the time it is placed in service.

At this point, the Developer cause HoldCo will also take out a new loan called “permanent debt” or “perm debt” and use part of the proceeds of that to pay off the construction loan they took out in Step 1 to initially build the project (the terms are better and is held by HoldCo, as opposed to the construction loan, which was held by the Developer directly).

Step 6: The Investor Starts Receiving Benefit

Once the project starts producing power and selling it to the utility company, it starts generating cash. This means that the investor is now getting four benefits:

A preferred return from the cashflows (this is part of the original agreement)

Their pro-rata share of any cash distributions in excess of the preferred return.

Any taxable losses or gains from the project, which will pass through to the investor. (And at the beginning it will mainly be losses due to accelerated depreciation).

The income tax credits, which can be used to offset the investor’s tax bill for as long as the tax credit remains in effect.

(The way this actually works is that, at tax time, HoldCo prepares a K-1 incorporating all of the above items, including the tax credits. This K-1 is then provided to HoldCo, which in turn prepares its own K-1, passing these items along to the tax equity investor, who then incorporates it into their own return).

This situation remains in place for a period of 5 years, after which the project undergoes something called a “partnership flip”, which we’ll describe next.

Step 7: After 5 Years, the Partnership Flip

Recall back in step 4 we asked why the Developer would be willing to give 99% of the economic interests in HoldCo to the tax equity investor even though the investor was only putting ~30% of the project purchase price? In this step we find out why.

As you may (or not) know, in a partnership the allocations of income (in the accounting sense) and cash can be separated and can be changed at any time. In short, in a partnership flip, the tax equity investor’s allocation of cash and income vs the Developer’s allocation “flip”: whereas originally the split might have be Developer 1% / Investor 99%, by the end of the flip it’s usually something like Developer 95% / Investor 5%.

After the flip, the tax equity investor still owns some residual amount of the project. When the investor initially invested in HoldCo, however, a standard part of the deal usually gives the Developer the option to ‘buy out’ the investor at a predetermined price and take full ownership of HoldCo (and hence the project). At this point, the Developer will often exercise this option. The net result is that the project is now fully owned by the Developer and the investor is no longer involved with the project.

So now we clearly see the benefit to the Developer: whereas they did a lot of work upfront for relatively little benefit, they were able to build the project with cheap capital, and in the long run they gain ownership of the project for relatively little of their own money tied up.

From investor’s perspective, they got to take money that they were going to have to pay to the government in taxes (so a 100% loss), and instead invest that money in a project where they got a tax credit to eliminate that amount in taxes (i.e. ‘as if’ they paid)...but also get the additional pass-through losses, preferred return, cash distributions, and - in most cases - the buyout price. Plus, they can feel good that they invested in renewable energy, which benefits society as a whole. It’s truly win-win.

Details of Investment Timing

If you made it this far and are interested in potentially becoming a tax equity investor, there are a few further nuances that may be helpful to understand. This section reviews those topics.

Definitions

Before going further, it will be helpful to define a few key terms:

PPA (Power Purchase Agreement). The agreement that the project company enters into with the utility company to sell the power that it produces. PPAs usually specify the price of the power (in terms of dollars per killowatt hour, or $/kWhr) and are usually in effect for between 10-30 years (20 is common).

MIPA (Membership Interests Purchase Agreement). This is the agreement by which the HoldCo (jointly owned by the Developer and the tax equity investors) buys the interests in the ProjectCo from the Developer. We covered this in step 4c above.

EPC Agreement (Engineering, Procurement, and Construction Agreement). This is an agreement that the Developer signs with any contractors and/or subcontractors that will actually be building the project. You can think of this as the specification document.

Timing of Requirement Investment

In the example above where the tax equity investor invested $1 million, we assumed that all $1 million was invested at one time, up front. In reality, the actual commitment of capital takes place in stages:

Contractual Commitment (0%). Once the tax equity investor executes a subscription agreement, they are on the hook to invest but there is no upfront cash transfer.

Construction Completion (21%). At this step, construction of the project done but it hasn’t yet been connected to the power grid and so is not yet producing/selling power. It’s at this point that the investor needs to provide 21% of their committed amount. Why 21? Because by IRS rules one must own at least 20% interest in a project to be eligible to receive an allocation of tax credits.

Production Completion (69%). At this point the project is fully up and running, producing power, and selling it. By this point, the project has also reached a milestone called being “Placed In Service”, which is a term used by the IRS. The reason this is important is that the tax credits are initially granted in the year in which the project is “Placed in Service”.

Final Completion (10%). This isn’t so much a project milestone as it is a legal and financial one. At this step, everything has been put into place, and the K-1 provided by HoldCo has been reviewed and approved.

Risks

Risk #1: Project Overvaluation

The most detrimental risk to a tax equity investor is that, upon later review, the IRS judges that the assessed value of the project - and therefore the amount of tax credits given (which is based upon the project value) - was inflated. In this case, the IRS may reduce the amount of tax credits allowed - and possibly impose some penalty - causing the investor to owe back taxes.

This risk is mitigated by choosing a defensible valuation methodology and using reputable 3rd-party valuation firms. In our case, we use a very defensible discounted cash flow method based upon the power prices that will be locked in for the long term via the power purchase agreement with the utility company and good, science-based estimates on how much power the project is likely to generate based on location, average days of sunshine, sun intensity levels, etc. In addition, our projects are all evaluated by 3rd parties that do a lot of work in this space.

Risk #2: Tax Credit Disallowance

There are other reasons why some or all of the tax credit given to an investor might be disallowed retroactively; mainly that the IRS rules around ownership and timing weren’t followed property. For example, the reason the partnership flip happens after five years is because that’s the minimum amount of time that an investor must remain an owner in the project (after its “Placed in Service” date) to be eligible for the tax credit. If an investor were to drop below its 20% ownership prior to that, their tax credit would be invalidated and they may owe addition taxes retroactively.

This risk is mitigated by working with an experienced team that has managed many projects like this in the past and has strong legal and operational processes in place to ensure all rules are adequately followed.

Risk #3: Project Underperformance

The main benefit to the tax equity investor is the tax credits, but the additional upside comes from the equity in the project and the share of income that the project generates as it produces power. However, it’s possible that the project will not product as much income as expected. One reason for this no one can do anything about: if for whatever reason there isn’t as much sun as expected, not as much power is produced. The other reason is system failure or underperformance: perhaps a solar panel is defective or something breaks.

The way to protect against this is to make sure the Developer has significant experience in either managing operations and maintenance partners who monitor and maintain the systems, or do it themselves.

Q&A - Questions and Answers

Q: This seems too good to be true? Is it legal / legit?

A: Yes, the energy tax credit is clearly spelled out in Section 48 of the federal tax code. The paraphrased version says:

”...the energy credit for any taxable year is the energy percentage of the basis of each energy property placed in service during such taxable year...the energy percentage is...30 percent...”

Q: How do you find eligible projects to invest in?

In addition to our existing pipeline of our own projects (about $1.5 billion worth), if we don’t have enough available eligible projects of our own that still need to be funded, we can syndicate out your investment to other solar developers.

Q: Can the tax credits be ‘carried over’ from year to year?

A: Yes, for as long as the tax credit remains valid (i.e. Congress may pass legislation winding down the recognition of such credits).

Q: Why does the partnership flip happen after 5 years?

A: Five years is the minimum amount of time that an investor must remain an owner in the project (after its “Placed in Service” date) to be eligible for the tax credit. If an investor were to drop below its 20% ownership prior to that, their tax credit would be invalidated and they may owe addition taxes retroactively.

Additional Nuances

As mentioned previously, even the step-by-step guide above made some simplifications to make the process easier to understand. In this section (still a work in progress) we’ll talking through some additional nuances.

Developer vs Sponsor

In the step-by-step-guide, we talk a lot about the role of the Developer. In reality the developer typically is the one that is actually building the project, but the group that actually coordinates the tax equity component (i.e. the manager of the HoldCo) is usually know as the Sponsor. In our case, we are just both the Sponsor and the Developer, so we kept the initial explanation simple. However, in some cases where we may need additional projects to support your investment, we (as the Sponsor) may reach out to other Developers for projects.

Tax Credit Purchase

In the examples above, we assumed that if you invested $1, you got $1 in tax credits. In reality, the Sponsor will typically charge a little over $1.00 (say $1.15-$1.20). This helps the Sponsor offset some of its costs. Now because in the first year the project will likely generate losses (from depreciation) in addition to the tax credit, you are still going to get close to a 1:1 tax offset for every dollar you invest.

Detailed Tax Mechanics

The detailed tax and accounting mechanics for the ProjectCo, HoldCo, and Tax Equity Investor fund are beyond the scope of this article. For a more in depth explanation of the accounting mechanics (e.g. outside basis, capital accounts, reallocation of losses, etc.), please contact us. (This is probably most relevant for your CPA and/or Tax Counsel).